Insights

The Grid Snapshot of the Solana Ecosystem

The Grid Team

May 19, 2025

This report analyzes the Solana ecosystem using data from The Grid, a group committed to mapping the Web3 universe. Using AI assistance and structured data queries, we've created a comprehensive overview of our Solana ecosystem database as of May 16, 2025, when this data was taken from our API.

See full res image here.

Data Sources & Verification:

All this data is available at: solanareport.thegrid.id

Explore an interactive marketmap at: marketmap.thegrid.id

See all the Solana data here: solana.thegrid.id

We highly recommend using the API for machine access to the full dataset (rather than scraping our data): https://beta.node.thegrid.id/graphql - docs.thegrid.id

Limitations & Usage: While we strive for comprehensive coverage, The Grid is still in beta and continuously improving its data collection. All data is freely available to pull from our endpoint.

We welcome feedback and encourage users to tag @thegriddata when using our data for research or applications.

Editor’s notes (anything in italics):

For more pricing / on-chain information, see the Messari “state of Q1” report and this Blockworks dashboard. The Grid focuses on high-quality details on Web3 ecosystems, while pricing data is out of scope.

We hope you gain insights from our data and this report, and follow The Grid as we work to clarify our data. It’s still early.

Executive Summary: The State of the Solana Ecosystem (May 2025)

Based on data from The Grid Standard (TGS) as of May 16, 2025, the Solana ecosystem demonstrates robust growth and diversity across multiple dimensions. With 478 companies and 261 projects actively building, the ecosystem shows strong commercial maturity while maintaining grassroots innovation. Finance (183 profiles) and Infrastructure (103 profiles) form the backbone, while emerging sectors in AI (with 97+ AI-related products) and DePIN (57 products) represent significant growth vectors.

The ecosystem is predominantly active, with 636 active profiles (79%) and 1,015 live products (77%), signaling a healthy operational environment. Developer tooling (110 products) leads all product categories, reflecting Solana's emphasis on builder support. Interconnection analysis reveals key ecosystem enablers, including Jupiter, Step Finance, Dialect, and Wormhole, serving as critical infrastructure hubs.

Growth patterns show a 2021 surge (109 new profiles) followed by consistent annual development (59-72 profiles per year) through market cycles, demonstrating resilience. The token landscape features primarily utility tokens (223), with emerging innovation in liquid staking tokens and RWA tokenization.

Solana's competitive strengths lie in performance infrastructure, AI integration capabilities, and a thriving DePIN sector, positioning it for continued expansion in institutional adoption and cross-chain composability as network improvements like Firedancer mature.

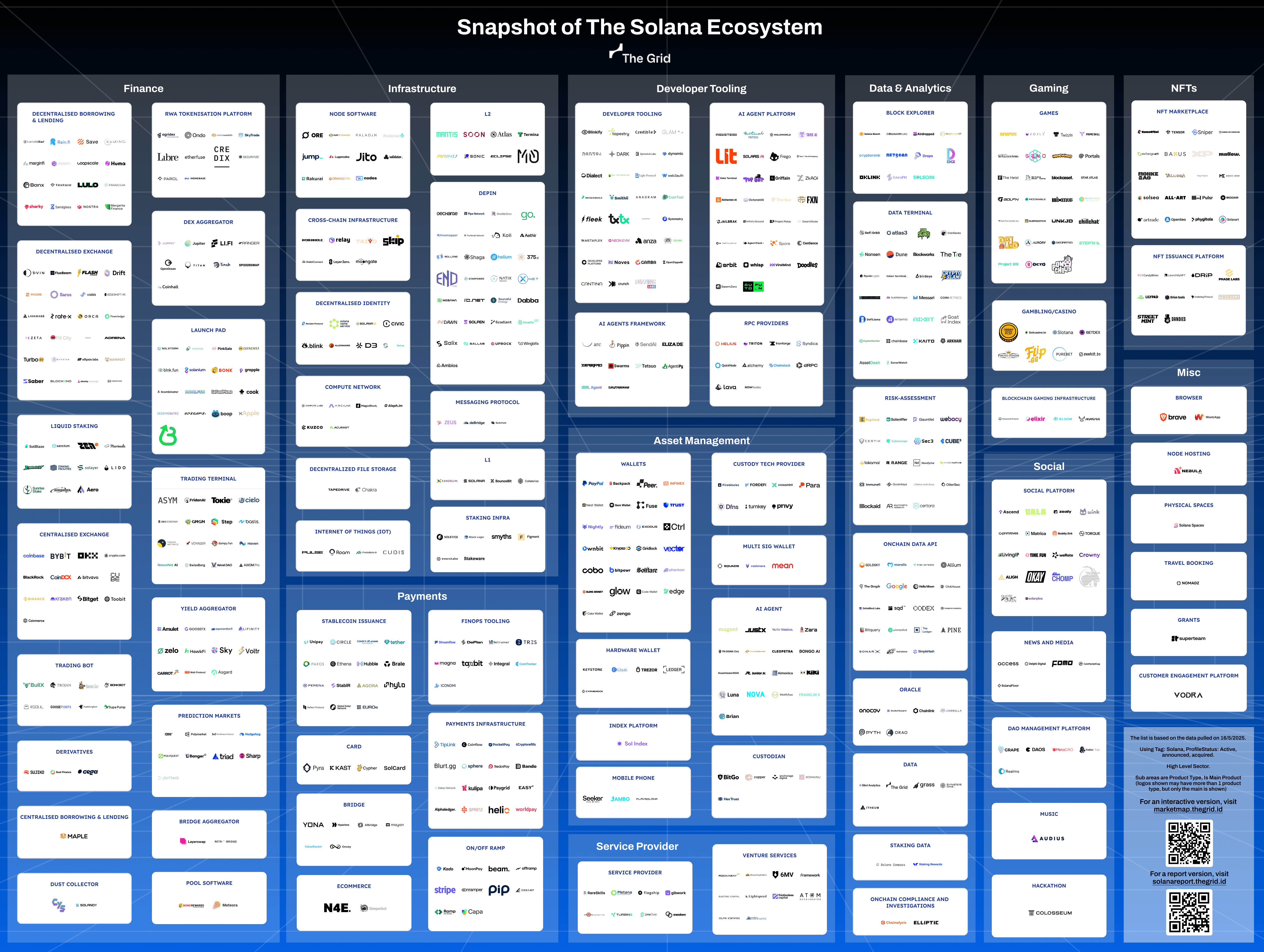

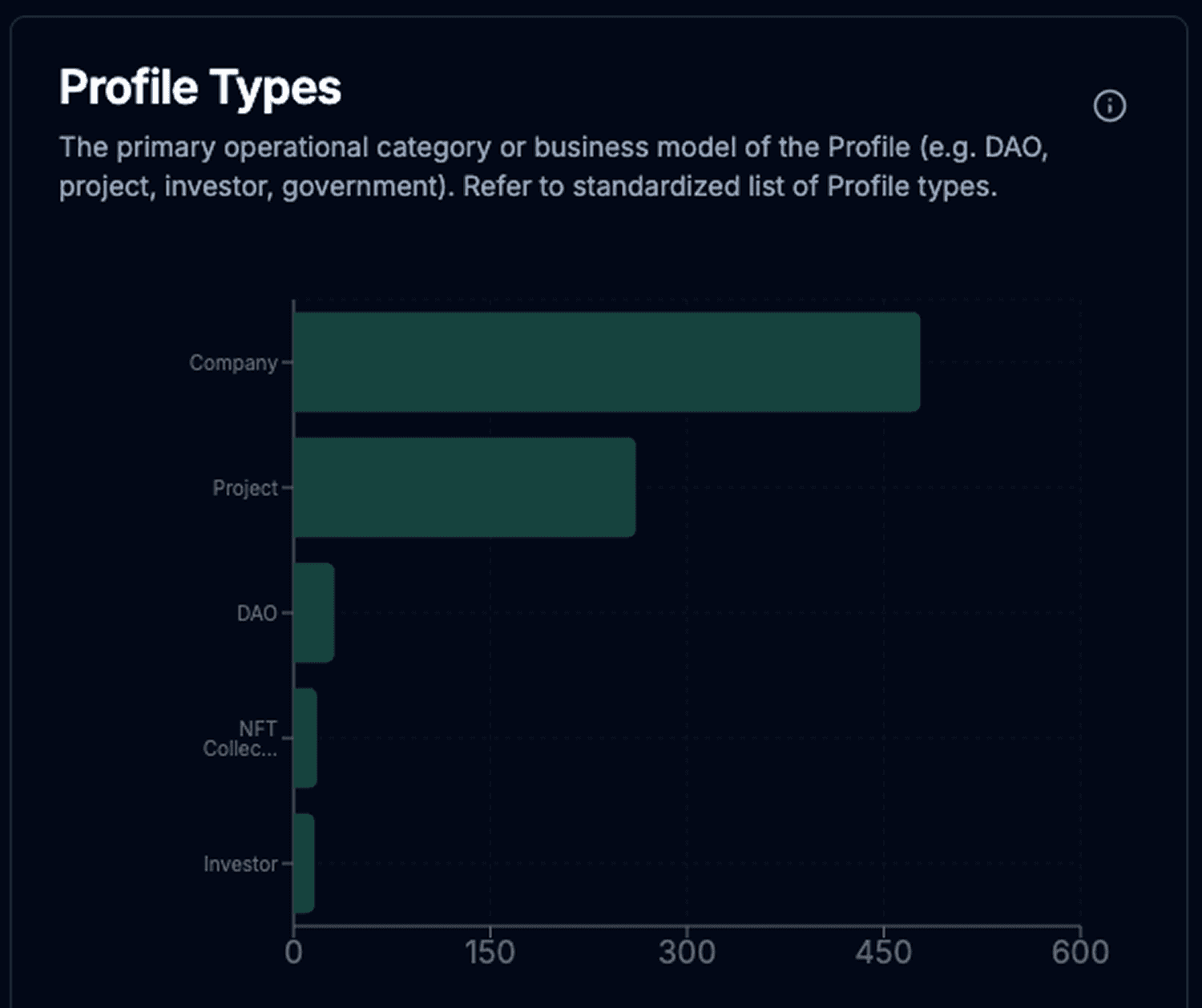

1. Ecosystem Composition

1.1 Profile Types

Companies: 478 profiles (59%) - indicating strong commercial presence and formal business structures

Projects: 261 profiles (32%) - signifying ongoing innovation and community-driven initiatives

DAOs: 31 profiles (4%) - showing adoption of decentralized governance models

NFT Collections: 18 profiles (2%)

Investors: 16 profiles (2%)

Researcher's Note: While many projects incorporate DAO elements, our current profile structure only accounts for entities explicitly categorized as DAOs in policy documentation. The limited number of investors reflected does not indicate lack of investment interest, but rather our focus on mapping profiles and their products, not investment rounds.

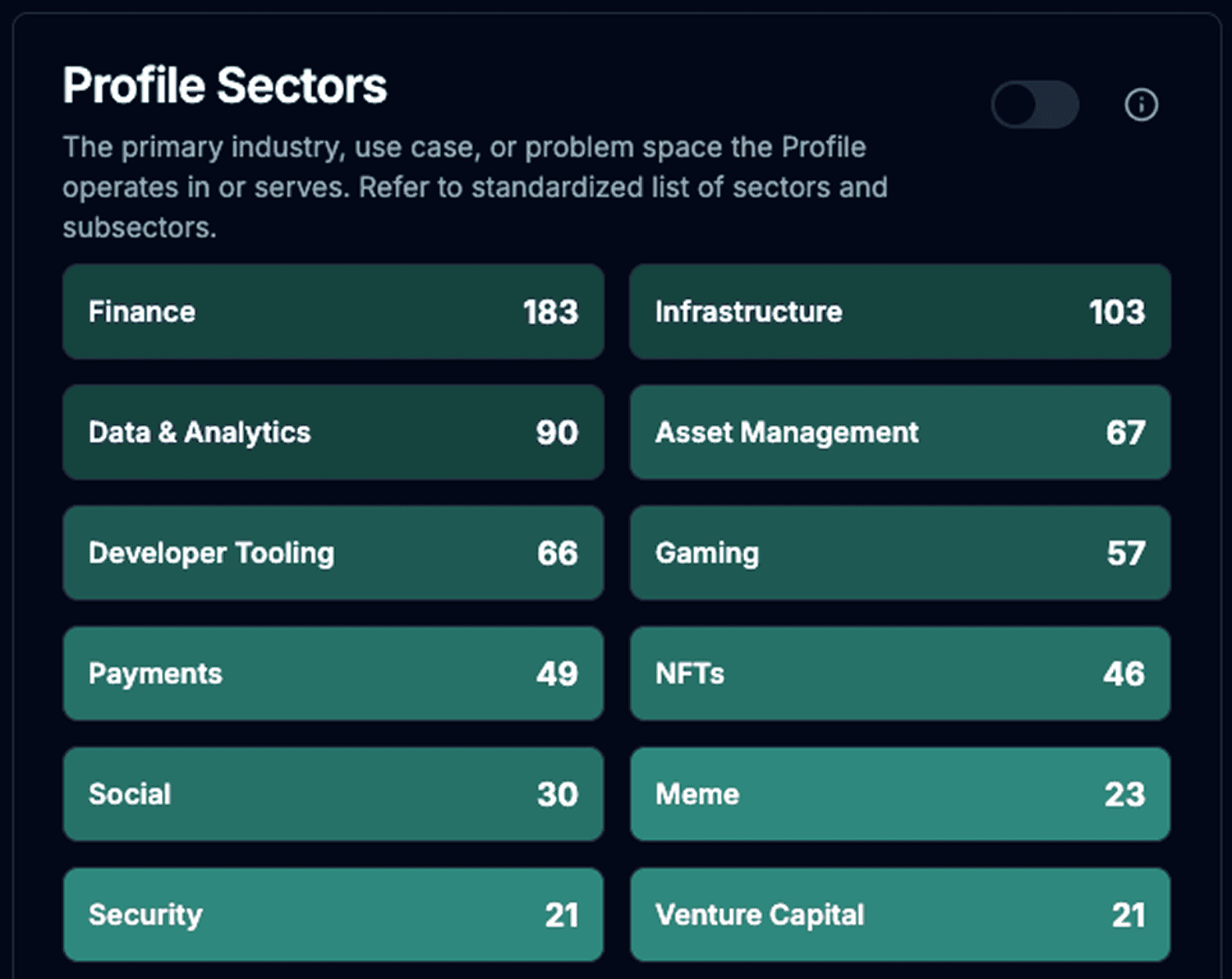

1.2 Industry Sectors

Top sectors: Finance (183), Infrastructure (103), Data & Analytics (90), Asset Management (67), Developer Tooling (66), Gaming (57), Payments (49), NFTs (46), Social (31), Meme (22), Security (21), Venture Capital (21).

The strong representation of Finance, Infrastructure, and Data & Analytics suggests a robust foundational layer, with growing focus on user-facing applications like Gaming and Social.

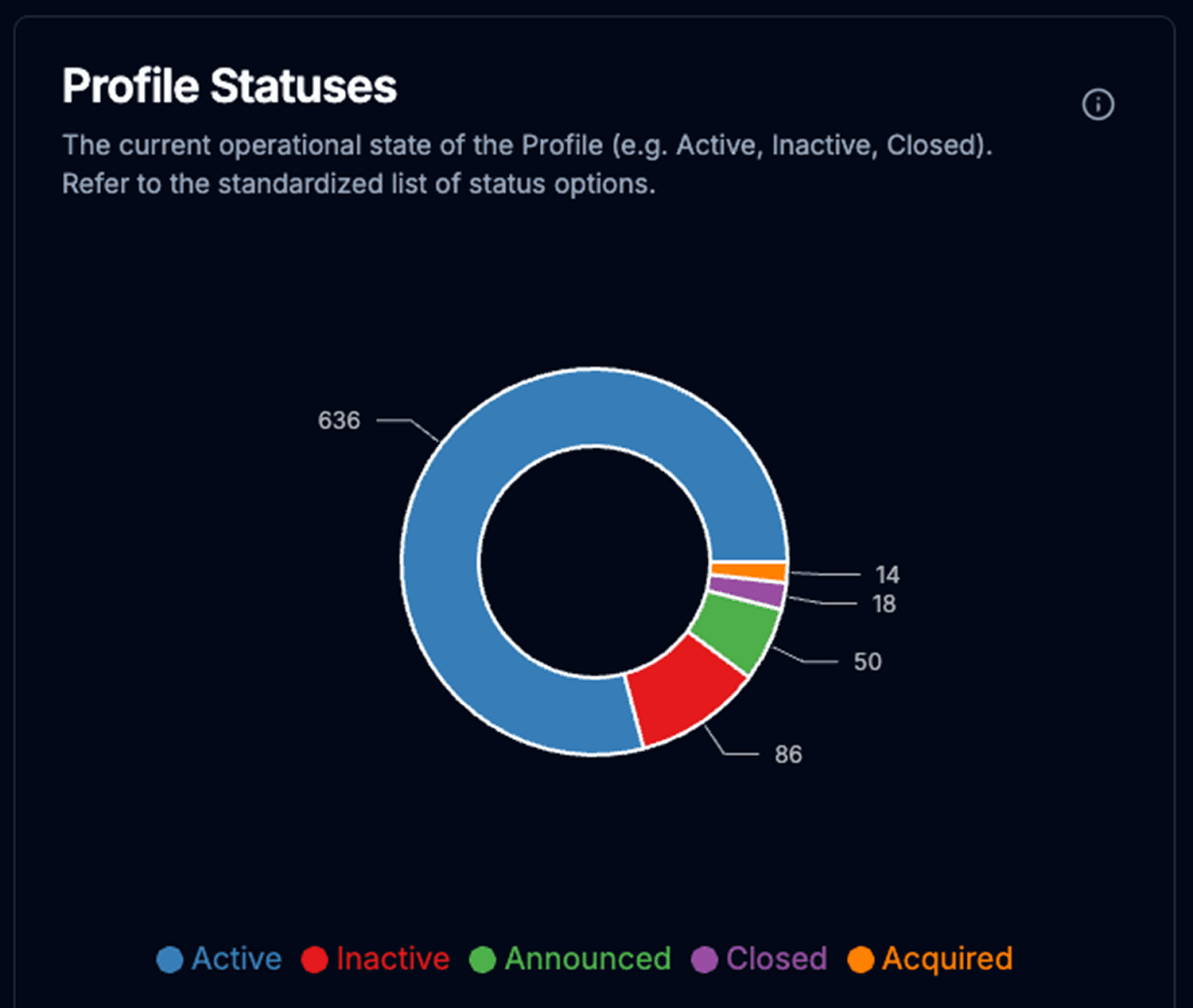

1.3 Activity Status

Active: 636 profiles (79%) - indicating a vibrant ecosystem

Inactive: 86 profiles (11%) - projects pivoting, pausing, or failing to gain traction

Announced: 50 profiles (6%) - representing the pipeline of new entrants

Closed: 18 profiles (2%) - ceased operations

Acquired: 14 profiles (2%) - indicating consolidation or successful exits

Methodology Note: Projects are marked inactive based on multiple signals, including ceased development, dormant social media, team departures, or official announcements. This conservative approach may undercount truly inactive projects.

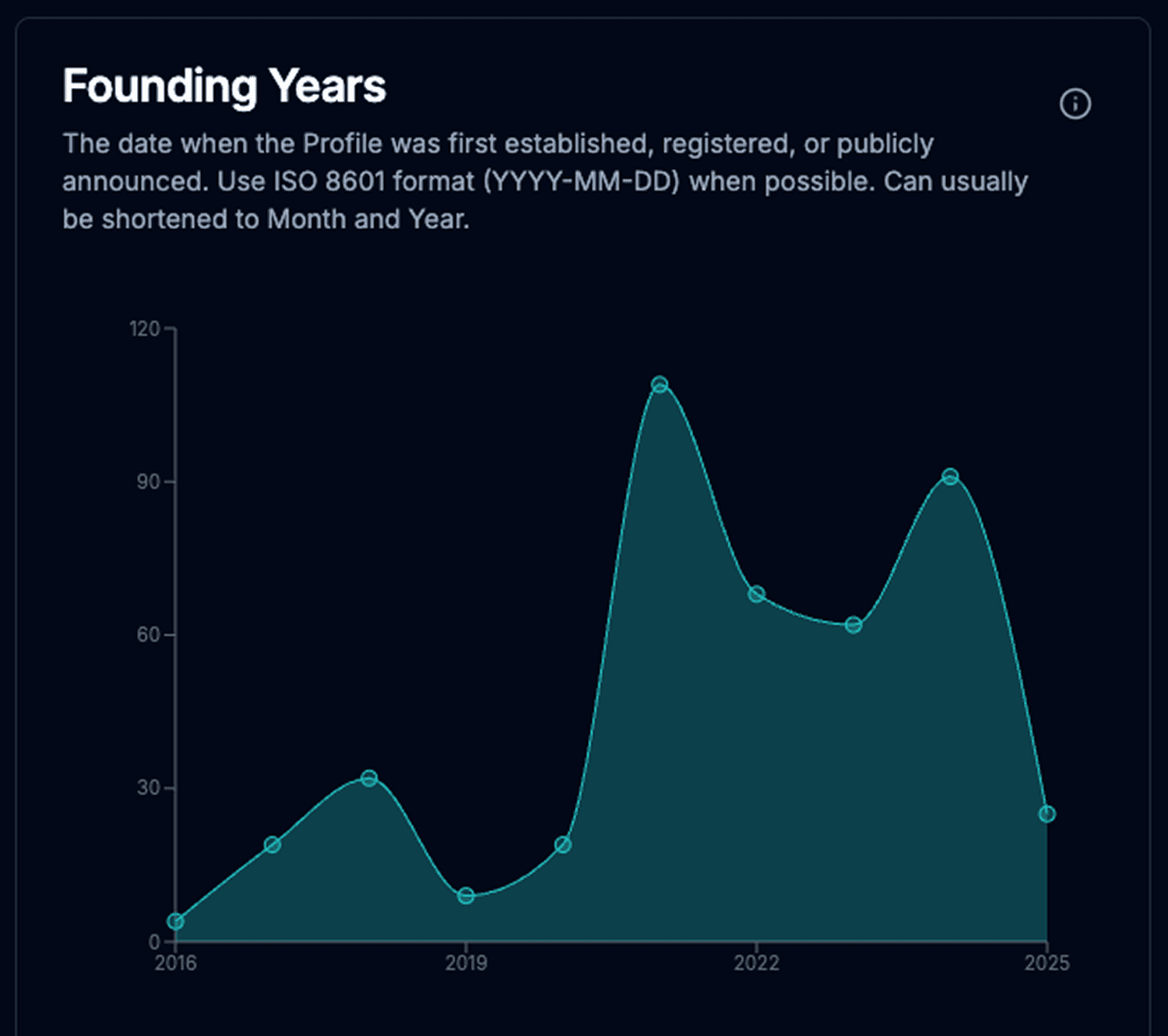

1.4 Historical Growth

Early Phase (2020): 42 profiles founded during Solana's genesis year

Growth Explosion (2021): 109 profiles (77 Companies, 17 Projects, 7 DAOs, 6 NFT Collections) coinciding with bull market conditions

Sustained Development (2022-2023): 125 profiles across both years, showing resilience despite a cooling market

Evolving Composition (2024): 70 profiles with Projects (44) significantly outnumbering Companies (26) for the first time

Current Year (2025 to date): 15 profiles, primarily Projects (9) over Companies (5)

Data Limitation Note: Founding date information varies in quality across profiles. This section only accounts for profiles with recorded founding dates, meaning nearly half are not reflected.

2. Product Landscape & Ecosystem Interconnections

2.1 Most Connected Projects

Top interconnected projects by connection score: SendAI (64) - AI agent development kit, Step Finance (43) - portfolio management, Dialect (37) - notifications framework, Jupiter (36) - DEX aggregator, AllDomains (29) - Web3 identity, Wormhole (26) - cross-chain messaging, Solana Name Service (26) - domain service, Awaken (26) - multifunctional platform, Crossmint (23) - NFT platform, Circle (23) - USDC issuer.

2.2 Connection Patterns

Ecosystem Enablers (23%): Projects providing fundamental infrastructure that many others build upon. Examples include Solana (supported by 662 products), Dialect (Blinks supported by 29), AllDomains (supported by 26), Solana Name Service (supported by 25), ElizaOS (supported by 15), and Metaplex (NFT standards).

Integration Hubs (31%): Projects integrating multiple services to offer comprehensive experiences. Examples include Step Finance (Dashboard supports 37 products), DEX Screener (supports 17), Alchemy (supports 40+), Chainbase (supports 15), Awaken (supports 25), and Backpack (supports 13).

Balanced Connectors (27%): Projects with substantial bidirectional connections. Examples include Jupiter (supports 4, supported by 16), Wormhole (supports 9, supported by 10), Phantom (supports 12, supported by 5), Circle (balanced support patterns), and SendAI (supports 32, supported by 28).

Limited Connection Profiles (19%): New/emerging projects, specialized niche projects, or profiles with incomplete data.

Note: Our dataset needs improvement in support relationships, and we're working to label primary relationships for all profiles.

2.3 Sector Analysis

Infrastructure Sector: Highest proportion of Ecosystem Enablers (42%)

Finance Sector: Highest proportion of Integration Hubs (37%)

Data & Analytics Sector: Most balanced distribution across connection types

Gaming Sector: Highest proportion of Limited Connections (31%)

AI Sector: Emerging pattern of highly interconnected products

This connection pattern analysis demonstrates a mature ecosystem with healthy distribution between foundation layers, integration services, and balanced connectors.

3. Product Types and Maturity

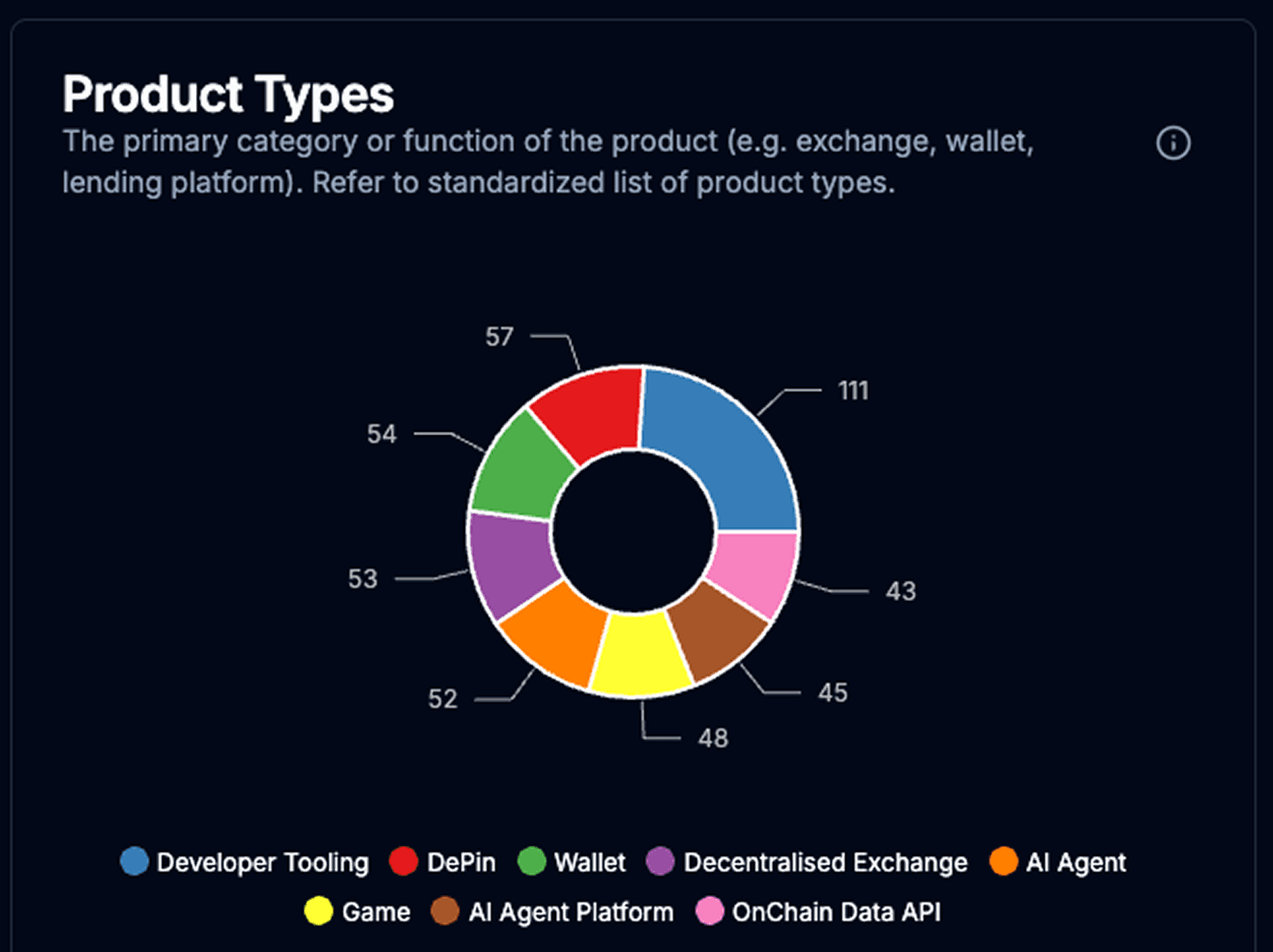

3.1 Product Type Distribution

Top product types: Developer Tooling (110), DePin (57), Wallet (54), Decentralised Exchange (53), AI Agent (52), Game (48), AI Agent Platform (45), OnChain Data API (43), Data Terminal (43), Risk Assessment (37), Payments Infrastructure (34), Decentralised Borrowing & Lending (34), Launch Pad (33).

The prevalence of Developer Tooling highlights a focus on enabling builders, while the strong presence of DePin, Wallet, DEX, and AI categories shows key areas of application development.

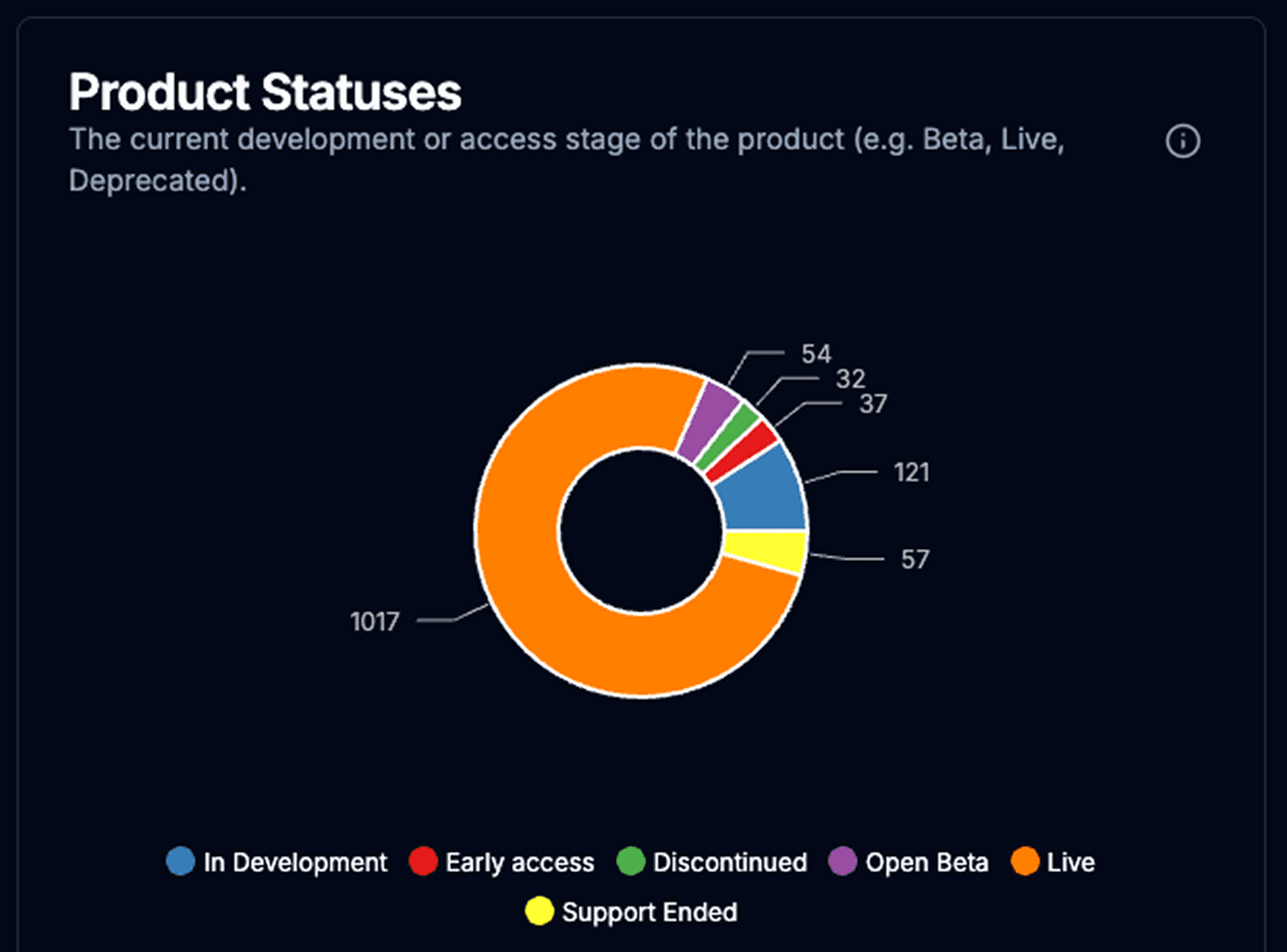

3.2 Product Maturity

Live: 1,015 products (77%)

In Development: 121 products (9%)

Open Beta/Early Access: 91 products (7%)

Support Ended/Discontinued: 89 products (7%)

The high number of Live products suggests a mature ecosystem capable of delivering functional applications, while the significant number of products in development and testing phases indicates continued innovation.

3.3 Emerging Trends

AI Integration (2023-2025): Rapidly growing with 115+ products across AI Agent, Platform, and Framework categories. Key examples include AIXBT (Nov 2024), SwarmZero (Mar 2024), Assisterr AI (Feb 2023), Daydreams (Jan 2025), and GoatIndex AI (Dec 2024).

DePIN: 57 products spanning pioneering projects like Hivemapper (Nov 2014), Helium (Apr 2014), and Render (Aug 2017), plus recent innovations like D3 (Aug 2023), io.net (2022), and AiNodes (Jun 2024).

Advanced DeFi: Complex offerings beyond standard DEXs and lending, including Yield Aggregators (23), Liquid Staking (20), RWA Tokenisation (17). Key players include Sanctum (Jan 2023), Kamino Finance (Aug 2022), Save (formerly Solend, Nov 2021), Marginfi (Sep 2021), and newer innovations like Haven (Nov 2024).

On-Chain Social (2023-2025): Rapidly emerging with SolMail, Banger (Mar 2024), Truth Terminal (Dec 2023), Luna (Jun 2023), Time.fun (Feb 2025), and Wink (formerly Only1).

Cross-Chain Infrastructure: Mature category of Bridges (13), Bridge Aggregators (4), and Cross-chain Infrastructure (15), with major players founded primarily in 2021: Wormhole (Jul 2021), LayerZero (Jan 2021), Allbridge (Jun 2021), and LI.FI (Jun 2021).

4. Asset Landscape

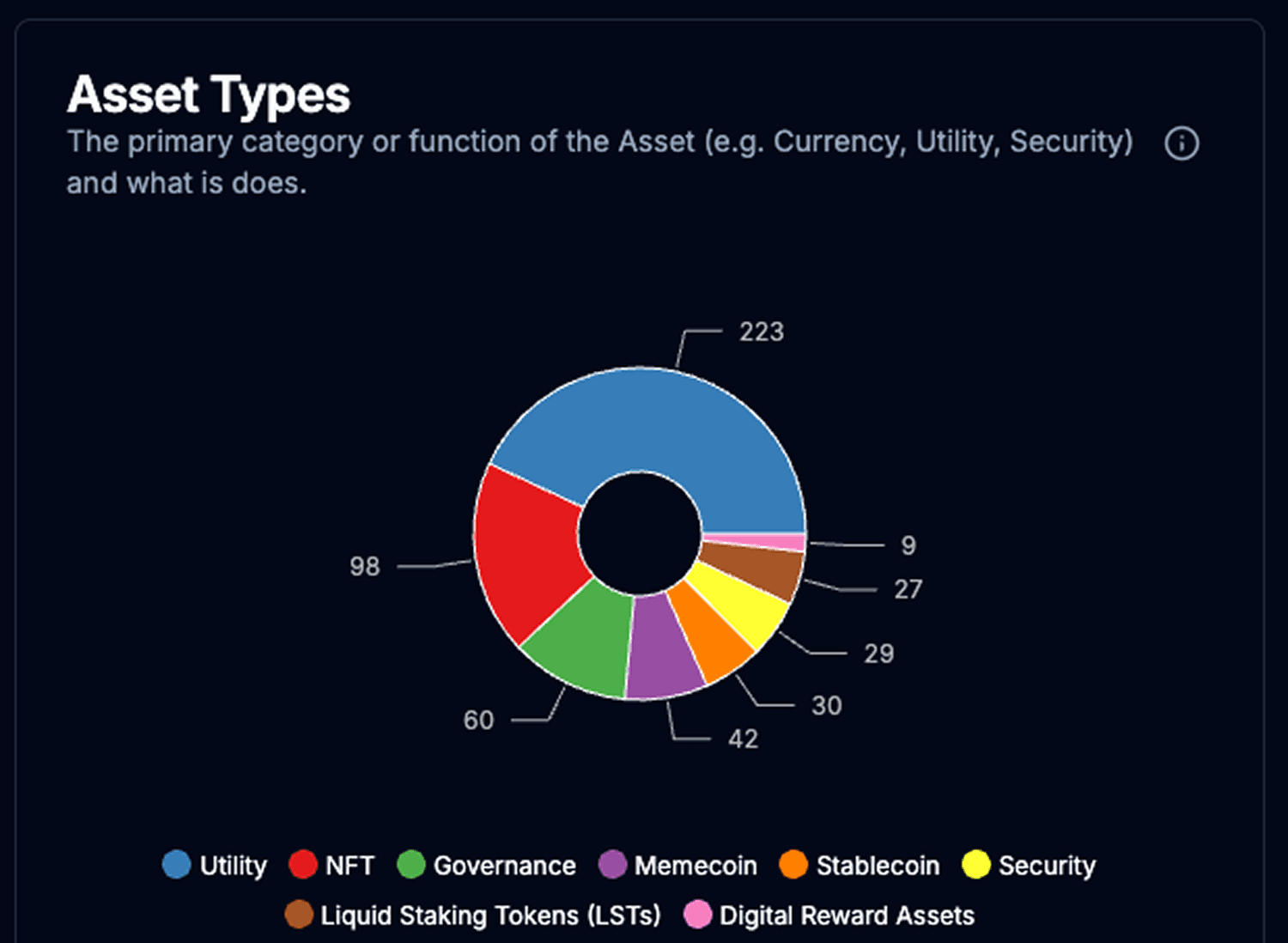

4.1 Asset Type Distribution

Utility: 223 assets (42%) - tokens with specific platform uses

NFT: 98 assets (19%) - unique digital collectibles

Governance: 60 assets (11%) - voting rights tokens

Memecoin: 42 assets (8%) - reflecting cultural trends

Stablecoin: 30 assets (6%) - price-stable tokens

Security: 29 assets (5%) - financial instrument tokens

Liquid Staking Tokens: 27 assets (5%) - growing DeFi segment

Others: 23 assets (4%) - including Digital Rewards, Wrapped Tokens, Currency, Restaked Tokens, and Synthetic Assets

Scope Note: This analysis intentionally excludes most memecoins unless they've achieved significant market presence or ecosystem impact, to maintain focus on substantive projects.

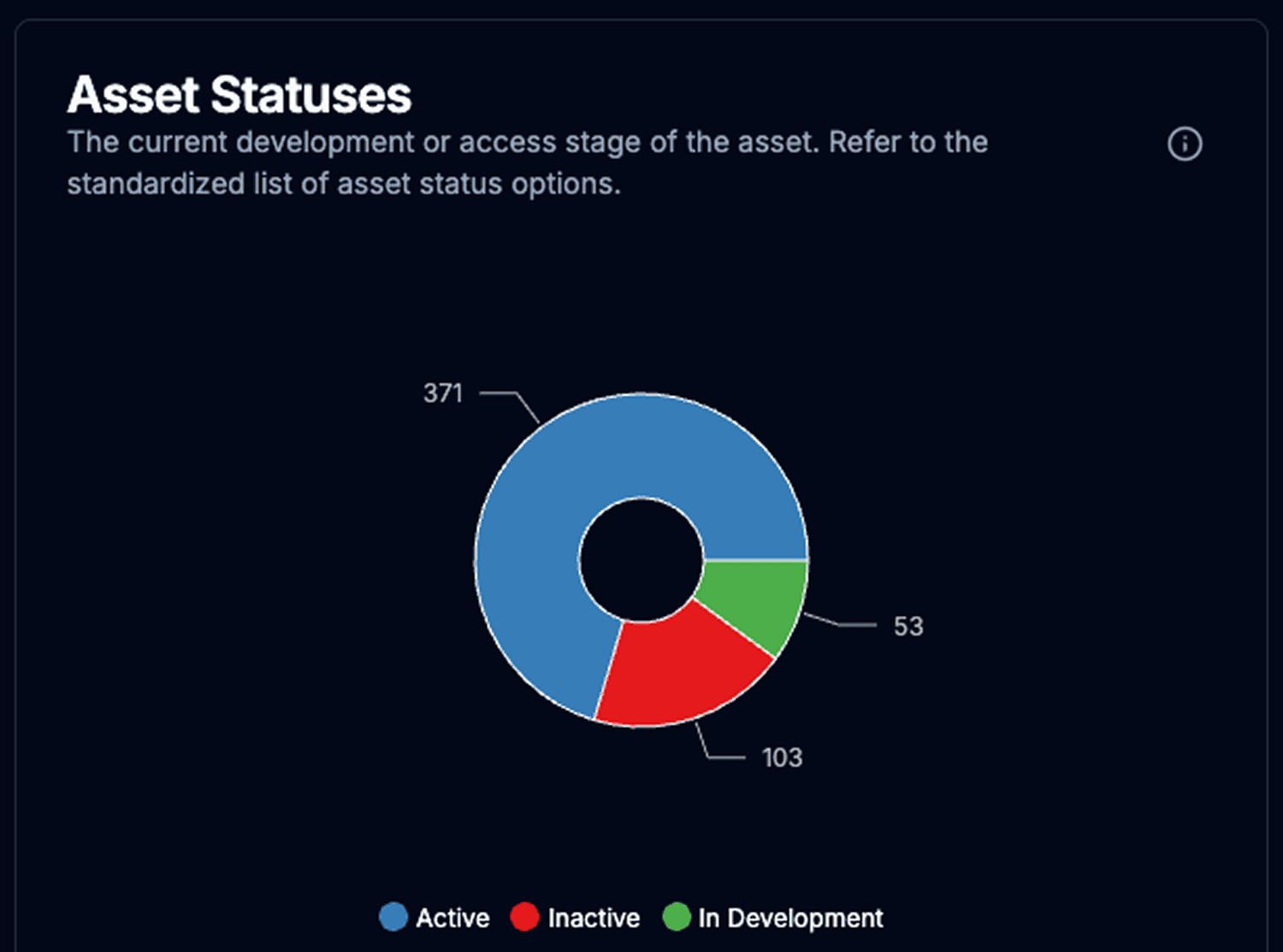

4.2 Asset Status

Active: 371 assets (70%)

Inactive: 103 assets (20%)

In Development: 53 assets (10%)

4.3 Token Innovation

Key innovations include Liquid Staking Tokens (27 identified, e.g., mSOL from Marinade or JitoSOL from Jito), Restaked Tokens (an emerging category with projects like Solayer), and specialized utility/governance tokens combining functions in unique ways.

5. Key Strengths

Performance and Scalability: High throughput architecture attracts DePIN, AI, and trading applications, enhanced by Firedancer development and L2s like Sonic.

Developer-Friendly Environment: Abundant tooling and infrastructure providers (Helius, Alchemy, QuickNode) create a supportive ecosystem. Innovations like compressed NFTs (Metaplex) and ZK compression (Light Protocol) lower barriers for specific use cases.

Vibrant DePIN Ecosystem: Leading platform for physical infrastructure networks (Hivemapper, Helium, Render), leveraging speed and low costs for managing large networks of physical devices.

Rapidly Growing AI Sector: Significant AI integration through frameworks like SendAI and ElizaOS, positioning Solana as a go-to platform for blockchain-AI convergence.

Strong Community Support: Initiatives like Superteam and various hackathons foster talent development and project incubation.